Global policy execution is needed for sustainable growth

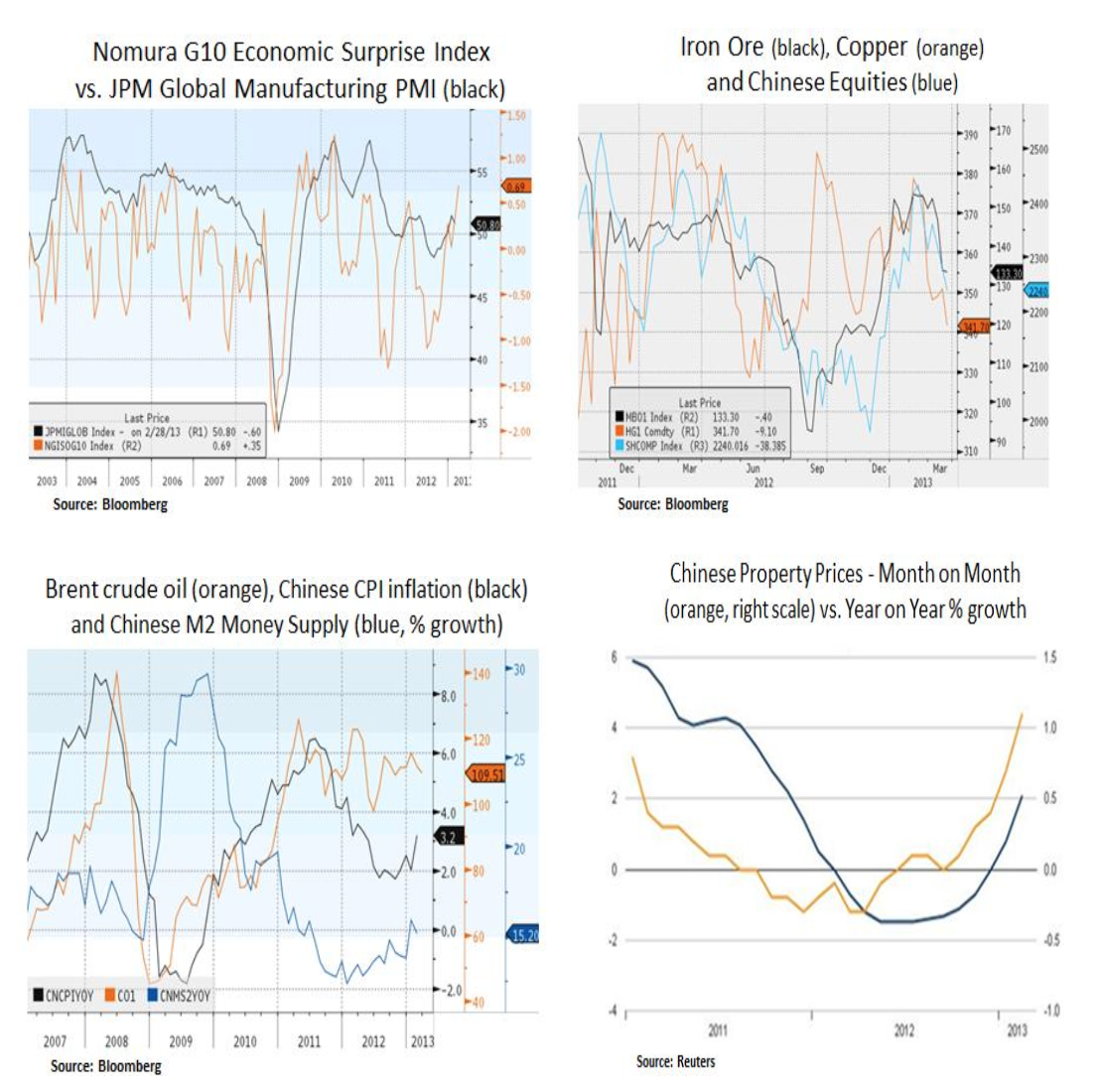

Financial markets continue to assess the balance of risks and opportunities across the global economy. In Europe, the markets witnessed in recent days a controversial rescue plan for the over indebted nation of Cyprus. One of the provisions of the plan included a 5.8bn EUR ‘haircut’ across the country’s depositor base. In the U.S., cyclical data are stable and declining public policy uncertainty is likely to instigate a capital spending recovery by year end. In Asia, concerns have been on the rise with regards to China’s challenging transition away from an investment led to a consumption driven economy. As such, we avoid base metal exposure such as iron ore and copper. From a portfolio perspective, we have been opportunistic in improving the risk-reward profile of our holdings. We maintain our balanced portfolio structure of income generating instruments and late-cycle/secular growth equities e.g. healthcare and software.

On the macro front, we are monitoring any policy shifts in the Eurozone’s strategy to resolve the ongoing growth and debt challenges. In our view, involving bank depositor losses in any ‘bail-in’ attempt constitutes a policy error by the Eurozone leadership i.e. it risks depositors’ trust in the Eurozone’s fragile banking system. As we mentioned in our last article, the European credit channel remains fragmented and credit creation in the southern economies remains subdued. In the face of rising non-performing loans and an inconclusive Italian election outcome, we expect the ECB to gradually catch up with its global peers with a more accommodative stance. A recovery in aggregate demand would be beneficial to large-cap U.S. multinationals e.g. in the technology and industrials sectors.

With regard to U.S. cyclical data, we are encouraged by the ongoing improvement in the labor market. At a time of extended fiscal and monetary policies, income growth is a key ingredient for consumer spending. In the medium-term, increased fiscal visibility will likely be a boost to business and household confidence. To a certain degree, we are pleased with the cyclical improvement in the U.S. budget deficit and we look forward to a future resolution to the country’s unsustainable entitlement spending. In terms of inflation risk, as we can see below, it is encouraging that money supply growth is not at exuberant levels. Thus, any interest rate hike expectations may stay tempered in an environment where economic growth remains in low gear due to fiscal consolidation in the coming quarters. In fixed income, we have a preference for low duration fixed income instruments (MBS) which would not be as sensitive to any interest rate volatility. Moreover, we avoid riskier segments of the credit market e.g. high yield corporate debt that has an unfavorable risk-reward profile.

In light of the Federal Reserve’s current two-day meeting, we do not expect any major shifts in the Fed’s open-ended quantitative easing program i.e. $85bn of monthly purchases of Treasuries and mortgage backed securities. Broadly speaking, liquidity is good for risk assets such as U.S. equities. The Fed’s ‘portfolio balancing channel’ favors dividend growing equities in a low interest rate environment; and whereby other financial instruments offer insufficient yield. To be sure, the Fed has stabilized the credit system especially at the time of the ‘Great Recession’ and has stimulated a housing recovery. As we can see below, most of the increase in the Fed’s balance sheet ends back at the Fed as excess reserves by the banking system. Thus, it is not surprising that the velocity of money is making new multi-decade lows. In other words, monetary base expansion does not necessarily lead to credit creation.

Lastly, we are monitoring the global growth backdrop which has been benefiting from ample monetary accommodation. We are mindful though of the delicate transition of the Chinese economy from a capital investment/export to a consumer driven economic model. Realistically, the transition will likely weigh on over- supplied base metals such as iron ore and copper. China is also facing some inflation pressures e.g. high pork prices and rising wages due to a contracting labor force. Moreover, excess credit creation by its shadow banking system seems to be fueling higher property prices. Therefore, we are observing the increasing concerns about a tightening PBOC monetary policy and we avoid materials equities with high operating leverage to base metal prices.

In conclusion, we continue to be opportunistic in improving the risk-reward profile of our portfolios. In a zero-rate environment we favor income generating instruments such as MBS and dividend growing equities. From a big picture view, we are cautiously optimistic with regard to the medium-term U.S. growth outlook and are respectful with regard to the structural or transitional challenges in large economic areas such as Europe and China.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.