September can be an inflection point for business confidence

Financial market participants enter September facing a busy calendar of important policy events. In the U.S., investors seek visibility with regard to the likely normalization path for the Federal Reserve’s monetary policy. In addition, investors look forward to the Fed’s leadership transition. On the fiscal side, Congress will have to strike the right balance between federal spending and debt sustainability. In Europe, after a tranquil summer, the market is anticipating more policy action after the German elections. In Emerging Markets, the arrival of renowned economist Raghuram Rajan at the helm of the Reserve Bank of India will likely give markets much needed policy coherence as India faces twin deficits, low growth and capital outflows. Arguably, geopolitical tensions in the Middle East are the biggest wildcard for the global economy and crude oil prices. Uncertainty over the above ‘known unknowns’ may create volatility in the short-term but increased visibility may give the corporate sector more confidence over the 2014 global growth outlook.

In the past month, U.S. equities faced elevated crude oil prices and a steepening Treasury yield curve. Despite elevated oil prices long-term inflation expectations have remained stable. Ahead of the Sept 17-18 Fed’s FOMC meeting, the market is focusing on the state of the labor market and the August payrolls report due on Sept 6th. As we can see below, our labor conditions indicator and the level of initial jobless claims seem to point to further improvement in the labor market. Moreover, the August ISM manufacturing report has given an encouraging leading signal with regard to industrial production in the coming months. If indeed the economy is on a firmer footing, the Federal Reserve is likely to embark on its normalization path this month. Thus, there is still some Treasury yield curve steepening risk and we continue to avoid long duration fixed income classes.

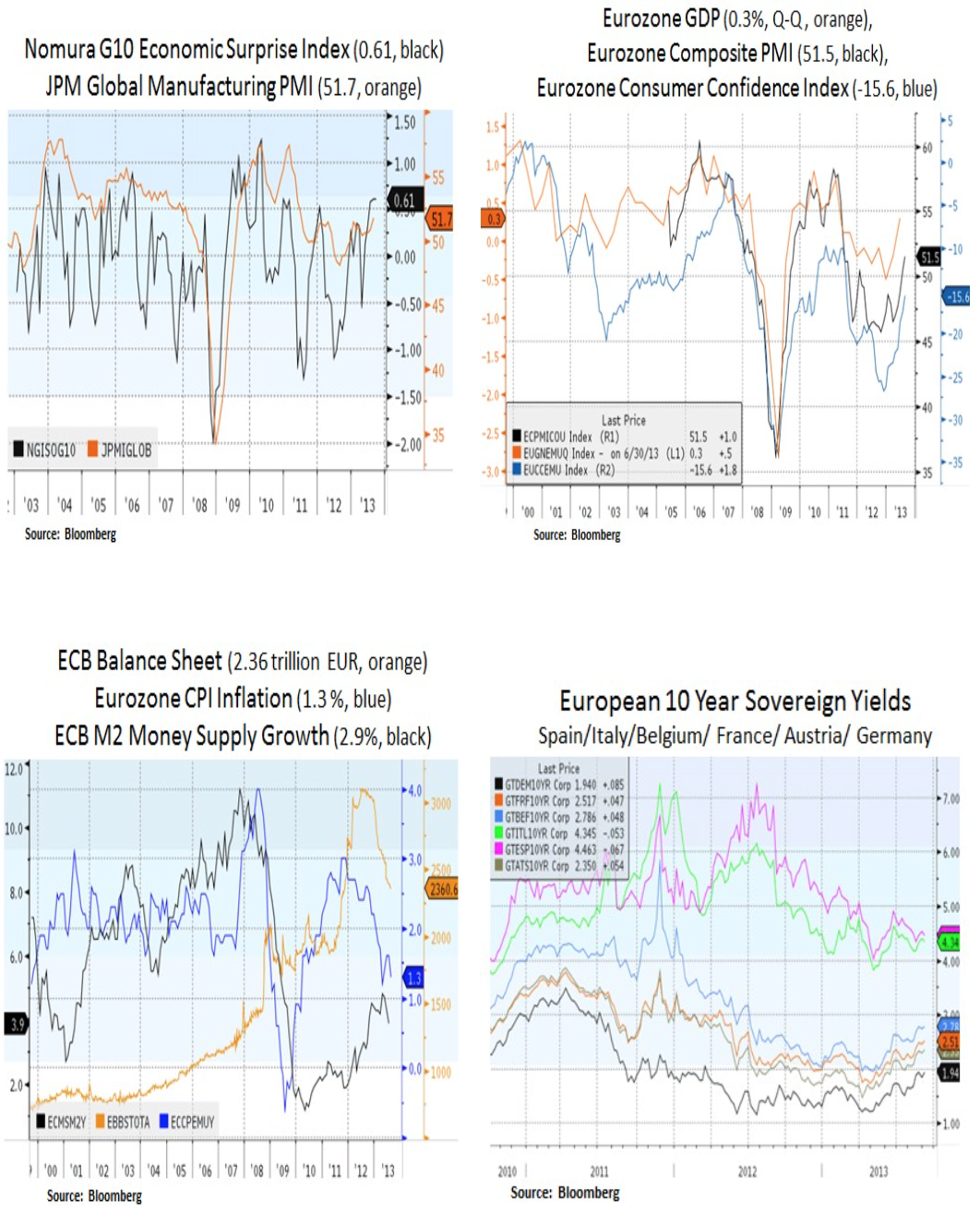

On the global manufacturing front, developed market economies and China have continued to show sequential improvement. Europe in particular has continued to show broad based cyclical traction and the Eurozone’s GDP expanded in Q2 2013. The U.K. in particular has witnessed a strong rebound in domestic demand and exports. The positive feedback loop in Europe could continue to gather momentum after the German elections. From an equity perspective, we favor exposure in late-cycle industrials and large-cap technology companies that can benefit from a rebound in enterprise and capital spending.

As we can see below, with inflation in check, the ECB has more capacity to assist with the Eurozone’s nascent economic recovery; especially in peripheral economies that face tight private sector lending conditions. To be sure, more needs to be done with regard to bank recapitalizations and domestic reforms in peripheral economies. In addition, the Eurozone has more operating leverage to global growth prospects and emerging markets. Apart from capital outflows in Southern Asia, we note that the recent growth stabilization in China has benefited from further expansion in credit and infrastructure spending. Therefore, we’ll continue to assess the sustainability of the current cyclical traction in global growth and whether developed economies can display more leadership.

In conclusion, September is likely to be an important month as CEOs and households gain more visibility over the 2014 U.S. and global growth outlook. Federal Reserve policy normalization, global liquidity conditions and geopolitical tensions are points of focus in the coming months. With fairly low levels of capital spending and M&A activity we believe the current global business cycle has more room to run. Therefore, we seek to be nimble in allocating capital in times of uncertainty.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.