Policy action is likely to stem systemic strains

Financial markets remain in anticipation mode as June will be a very busy month for policy makers, in the face of ongoing systemic and cyclical risks. In the past two years we have witnessed cycles of complacency-crisis-response and as the stakes are rising we expect elevated policy action. In Europe in particular, in contrast with 2011, we expect the ECB to be even more aggressive in an attempt to safeguard the integrity of the European banking system. We also expect global central banks to stand by with globally coordinated swap lines which will facilitate the necessary USD funding to the European banking system. From a global growth perspective, easing inflation pressures are plowing the seeds for the next global cyclical leg which will be driven by emerging markets.

In Europe, divergent capital flows and sovereign borrowing costs are the source of systemic instability. In addition, uncertainty over the upcoming (June 17th) Greek election is also weighing on risk sentiment. The outcome of the election is difficult to predict but we believe the European leaders will continue to support Greece in order to prevent contagion to other European economies. In Spain, ultimately housing related bad debt needs to be restructured and it is plausible that a mechanism is put into place whereby the healthy banks are given a European life support and smaller insolvent banks go into a bankruptcy process. Thus, visibility over a sustainable Spanish banking system will likely halt the destabilizing deposit flight within the Eurozone payment system.

In the U.S., leading economic indicators still point to a moderate growth outlook. The May non-farm payrolls report pointed to softness in the labor market but the household employment survey showed strength (+422k), which is more consistent with recent consumer confidence readings.

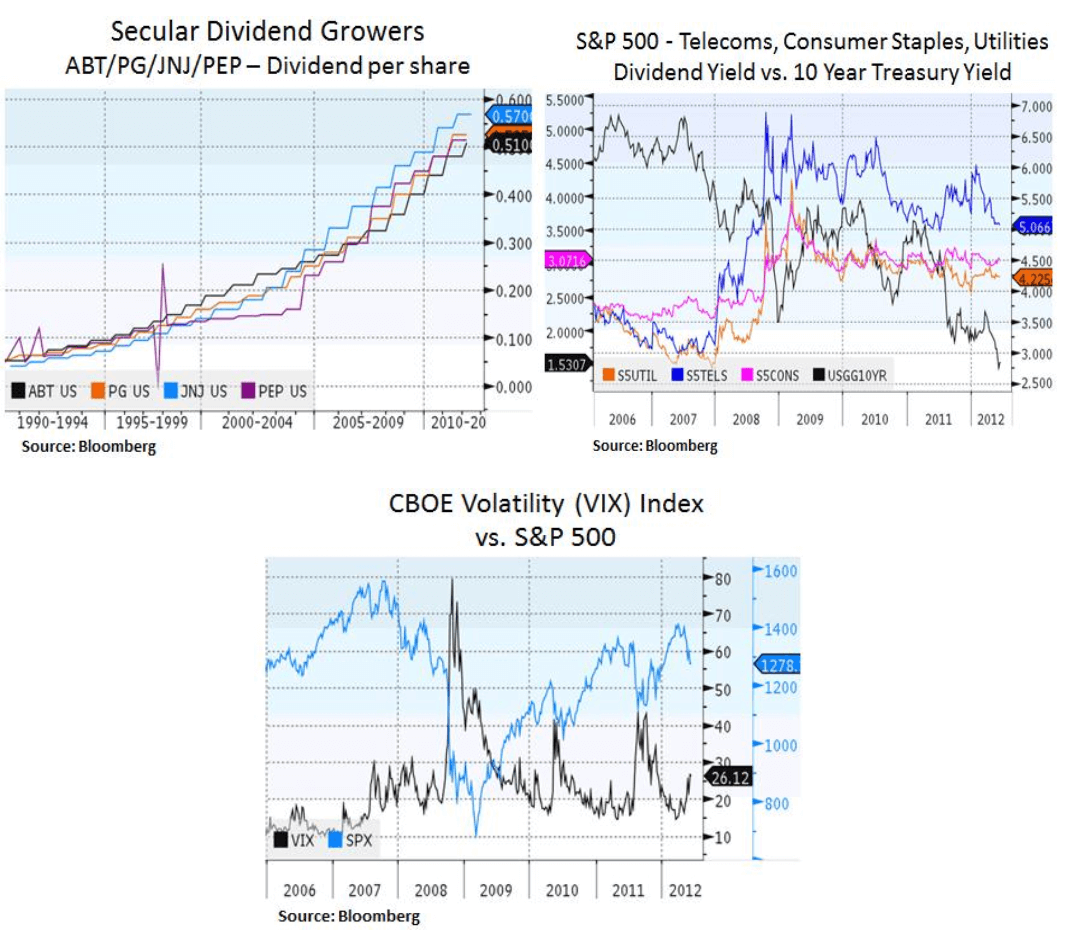

On the consumer side, low mortgage rates and easing gasoline prices are likely to be supportive of household budgets. This is especially vital at a time of lackluster wage growth. Moreover, as inflation expectations remain in check, the Federal Reserve is likely to stay in an accommodative mode. Slack in the economy remains significant due to high unemployment levels. From a corporate view point, low wage growth, easing energy prices and low interest rates are likely to keep corporate profit margins at elevated levels. Currently, profits are not being materially plowed back in the economy as investment expenditures. This is largely due to the 2013 fiscal uncertainty. Thus, in the medium-term, cash rich corporations are likely to sustain their capital allocations to shareholders in the form of growing dividend payouts and share buybacks.

In the past two years, declining inflation expectations as implied by the Treasury/TIPS market prompted the Federal Reserve to intervene in an attempt to stave off deflation fears and thus prop up corporate animal spirits by easing financial conditions. The Fed’s balance sheet has seen an extraordinary expansion since the crisis of 2008-9 and it is likely that the Fed will continue to keep rates low, especially with a view to stimulate the housing market i.e. the main asset for households. The Fed’s own assessment of GDP growth is gradually becoming more realistic and along with easing inflation expectations the Fed may be gaining some leeway for further action. The Federal Reserve chairman has been very explicit with regards to the 2013 fiscal risks and the Fed’s inability to fully offset an economic drag due to fiscal consolidation. Therefore, Congress holds the key to the pace of fiscal contraction and the market is eagerly awaiting visibility on a sustainable Federal budget outlook.

We are more constructive on the outlook for emerging market growth whereby economic fundamentals have more solid underpinnings than developed market economies e.g. unlevered sovereign and household balance sheets. In contrast to 2011, emerging markets are now witnessing declining energy and food inflation. Easing inflation pressures are granting national central banks with more latitude over monetary easing. As emerging markets rebalance their economic models to more domestically driven growth, we expect their secular growth path to resume and ultimately lead global economic expansion. This resumption in growth will likely be an earnings boost to U.S. multi-nationals e.g. in the energy, industrial and technology sectors.

In conclusion, we continue to assess the risks and opportunities in the marketplace. In a period of elevated uncertainty, our investment strategy remains income oriented (MBS, preferred shares) and we lean on large-cap dividend paying equities that offer cash flow and earnings visibility. Lastly, from a bottom-up perspective we seek to take advantage of favorable risk-reward opportunities that episodes of market volatility create.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.