Powell Squashes Hopes of a Pivot

It has been a tumultuous year for financial assets. Negative macroeconomic trends including persistent global inflation, a surging U.S. dollar, tightening monetary policy, and decelerating consumption have weighed on markets in 2022. The generational high in inflation has led to decades of market experience being challenged, with stocks and bonds commonly falling together. This year has seen a peak-to-trough drawdown of over 25% in the S&P and a 15% drop in Treasuries. U.S. bond yields have hit new multi-year highs as markets brace for more central bank rate hikes. That has kept equities pinned near two-year lows despite occasional bear market rallies like the one that saw the S&P bounce over 8% in the month of October alone.

Equities’ recent bounce may reflect rotation into value and anticipation of a future Fed pivot. EPS beats have been greeted by rare negative price returns this earnings season. The October rally was driven in part by P/E expansion as the earnings outlook has been deteriorating, suggesting the equity market was likely trading on prospects for a Fed pivot rather than a better-than-expected earnings outcome.

These pivot aspirations were dashed during Fed Chair Powell’s hawkish press conference yesterday. The Fed hiked 0.75% as expected with the statement adding language about accounting for “cumulative tightening” and “lags with which monetary policy affects economic activity and inflation.” Which can safely be interpreted for a slowdown in the pace of tightening soon. Meaningful core inflation readings since the September meeting justify the outsized hike. What the markets did not like however was Powell’s comments that if the Fed did over-tighten, it could use its tools to adjust, but the cost of not going far enough could mean inflation gets entrenched.

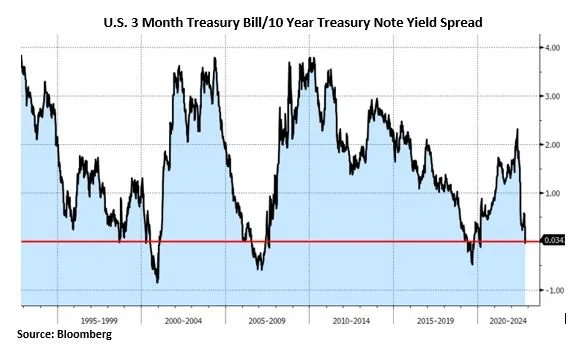

The most predictive yield curve for recessions, the 3 Month bill/10 Year note, had inverted and generally leads recessions by about nine months. This is a metric that Chair Powell has said he is watching as a sign the Fed has gone far enough. Federal Reserve officials signaled their aggressive campaign to curb inflation could be entering its final phase even as they delivered their fourth straight 75 basis-point interest rate increase. While central bankers said that “ongoing increases” will still likely be needed to bring rates to a level that are “sufficiently restrictive to return inflation to 2% over time,” the acknowledgement of both the lags and cumulative effect of the hikes was notable.

Equities usually do well after U.S. midterm elections. Gridlock is common and prevents policy change that could create uncertainty in equity markets. That may not hold true this time around due to the expected recession from the Fed tightening financial conditions. Weak 3rd quarter earnings hammered some of the biggest tech stalwarts, yet despite this, the S&P 500 managed to hold its gains at the time. The earnings reports have blamed the weak macro backdrop with a combination of FX headwinds, slowing consumer demand, weaker advertising, cost cutting, and inventory buildup.

Looking abroad, the sharp drop in Chinese equities and capitulation in the Yuan strongly hint that there is further trouble for the economy. President Xi appointed loyalists into key positions signaling a plan to maintain the status quo in terms of zero-Covid policy, which was a significant disappointment to investors.

Rising interest rates have dominated the market story in 2022 and have led to a historically poor performance of the U.S. Treasury market. Credit spreads however have remained relatively muted given the broader environment. Credit markets could be the next shoe to drop as liquidity in the system is drastically reduced.

There will be two more CPI and jobs reports before the next FOMC meeting in December. Sustained inflation and labor market strength will make it difficult for the Fed to slow the pace of rate hikes. We expect markets to remain volatile as investors interpret economic data in the hopes of determining the Fed’s future path of rates.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request