Playing Catch-Up

Markets were unkind to investors in September as the S&P 500 and Barclays U.S. Bond Aggregate Index both fell over 9% and 4% respectively. The violent gyrations came as market participants wagered whether hawkish policies by global central banks will ultimately result in a recession and earnings contraction. Due to inaction from central bankers during the pandemic recovery, they are now faced with an unenviable tradeoff. They must continue to hike rates to tame inflation at the cost of economic growth.

UK gilts (government bonds) yields reached 14-year highs before the Bank of England intervened by buying long-term bonds to stabilize markets and halt the selloff. Fiscal authorities in the UK tried to boost growth with the largest unfunded tax cuts in 50 years and spending increases. As a result, the pound plummeted to all-time lows and stocks sank. A crisis was triggered by the speed with which longer gilt yields rose prompting margin calls on UK pension funds and fears of a “Lehman Moment” contagion risk amidst pension fund insolvencies. This served as a stark warning to all major central banks that financial stability concerns are manifesting in unpredictable ways.

Meanwhile, yields on 10-year U.S. Treasuries topped 4% for the first time since 2010. As can be seen in the MOVE index, which is a weighted index of implied volatilities of Treasuries across the curve, bond volatility has been significant. There appears to be a fundamental mismatch in the Treasury market. As deficit spending has driven up the U.S. government’s debt, the value of publicly traded Treasuries has ballooned to more than $23 trillion. This dwarfs the resources of the group of large dealer banks that, as market makers, are supposed to facilitate orderly trade in this market. As a result, the dealers are at times unable or unwilling to handle the volume of trades that investors seek.

The U.S. dollar has surged as international investors seize on higher U.S. interest rates from the Fed’s most aggressive policy tightening since the early 1980’s and seek a haven from market turmoil. The rally is exacerbating the economic difficulties of nations around the world by pushing up prices of imported food and fuel. That’s putting further pressure on many central banks, which have been raising their own interest rates in an effort to cool the surge in consumer prices. The strong dollar is also a drag on American corporate earnings by reducing the value of money made abroad. Companies like Microsoft have warned that a stronger dollar is hurting the bottom line when it cut its outlook in June. The strength in the greenback is also forcing foreign buyers of U.S. corporate debt to sell in order to hedge their risk. Foreign investors faced with low-yielding debt were lured into dollar debt earlier this year because of the attractive relative yields. Hedging currency exposure is now getting too expensive for many of them. Japan spent roughly $20 billion on its first intervention since 1998 to bolster its currency, where unlike the Fed, the Bank of Japan has been keeping interest rates low.

Central banks are trying to do whatever it takes to tame inflation, but they haven’t acknowledged that they will have to sacrifice economic growth in order to achieve that. Many believe that central banks will stop hiking next year and not go as far as necessary to get inflation back to target quickly. We’ve already seen the Royal Bank of Australia (RBA) raise their key rate this week by less than was expected, and other central banks will likely follow suit and live with inflation once confronted with economic damage; either in the form of recession, financial instability, or both. That in turn has supported the narrative of a Fed pivot. While a less-hawkish monetary backdrop apparently has provided some of the fuel for the financial asset rally we witnessed earlier this week, one should take caution in mistaking overdue short-covering with a positive shift in the fundamentals.

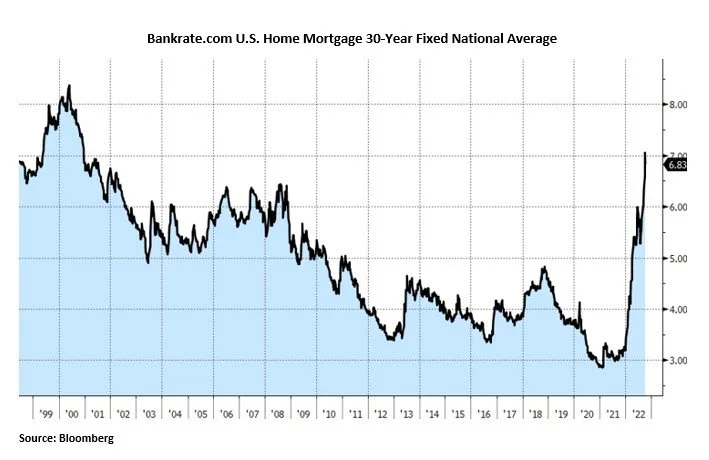

The deciding factor for the Fed is the labor market. Small cracks are showing, with more anecdotes from large companies telling of hiring freezes or layoffs, and rising numbers of people working part-time for economic reasons. Earnings have been resilient, but are likely to show a rollover in the third quarter. With mortgage rates at multi decade highs and pending home sales at their lowest level since 2011, housing is likely to struggle. Equities still face margin compression and lowered earnings estimates which leaves them vulnerable as well. So, in the end, the Fed is likely to get what it wants, but because they’ve been playing catch-up and have been forced to hike as quickly as they have, it’s likely at great cost. Once again, market chatter is growing that the Fed won’t be able to raise rates to the 4.6% terminal rate it projected in the latest dot plot. As activity softens towards contraction, the Fed is likely to become more data dependent particularly as political pressure on them mounts.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request