Public debt sustainability is essential for durable growth

Investors continue to allocate capital in an environment of low economic growth and public policy uncertainty. The biggest driver for risk asset performance in 2012 has been the ongoing monetary support by global central banks. Abundant liquidity and low interest rates have reduced systemic tail risks in developed markets and risk asset volatility has been subdued. From a cyclical perspective, the global growth backdrop remains mixed with some tentative signs of bottoming growth in Asia and Europe. The challenge at this stage of the post-credit crisis recovery is the delicate task of normalizing fiscal policies without hampering growth. Thus, policymakers are trying to estimate the potential negative multiplier effect to economic growth as fiscal policy tightens. In a near zero rate environment, it is likely that central banks such as the Fed and the Bank of Japan will take further unconventional monetary measures in 2013 in an attempt to stimulate growth.

Financial markets are currently focusing on the timing and duration of U.S. fiscal negotiations. From our lens, a fiscal deal reduces uncertainty but the nature of the deal is equally important i.e. what will be the optimal mix of tax increases and federal spending cuts. Ideally, money flowing in the private sector is the best course of action as the private sector is the better allocator of capital. Thus, there is a risk that higher than expected tax increases and fewer federal spending cuts will be perceived as a sub-optimal deal for growth. Moreover, the fiscal deal needs to address public debt sustainability in order to provide businesses and households the necessary confidence to invest and consume respectively.

One of the key metrics to monitor in 2013 is inflation expectations. Near-term inflation is likely to remain in check as a result of lower energy prices, subdued labor costs and soft economic growth. Looking ahead though (5-10 years), financial participants will likely try to handicap any inflation turning points and potential consequences on debt and equity assets.

A change in inflation expectations is potentially a hurdle to a substantial expansion to central bank balance sheets. As we can see below, expansion of the monetary base in a deleveraging economy is not as effective i.e. excess bank reserves are not turned into credit. Moreover, investors are interested in gaining visibility into the Fed’s exit strategy i.e. how the Fed’s balance sheet and interest rate policy will be normalized over time. Therefore, monetary policy is not a perpetual panacea and the policy baton has to be passed to the fiscal authorities at this stage of the economic recovery.

Labor costs are the biggest component of company cost structures. The November U.S. payroll report indicated an ongoing sluggish labor market with subdued wage growth. Most concerning is the ongoing trend for employment growth skewed to the > 55 years of age cohort. This is a result of the loss of wealth during the 2008-9 crisis. Therefore, we remain cautious on the U.S. consumer, as the more productive age cohort of 25-54 is experiencing insufficient income growth and as the baby boomer generation is retiring.

On a more positive note, we are encouraged by the recent decline in gasoline prices and the robust U.S. energy sector prospects. The U.S. energy sector has the potential to overtake its main global peers in terms of energy production and it is plausible that the U.S. will achieve energy independence within the current decade. As the global oil and gas shale revolution continues, the U.S. energy sector remains at the forefront and we have a favorable view on the U.S. oil services industry as it has the technological edge that enables the exploration of untapped geological formations. Moreover, from a global inflation point of view, we are encouraged by the steady global oil production. This production profile is likely to keep global headline inflation concerns in check.

On a further positive note, we are encouraged by the ongoing healing in the U.S. housing sector. At a minimum, we expect housing prices to recover gradually. This is beneficial for household wealth perception and the health of the U.S. banking system.

On the European front, we are encouraged by the recent pick-up in the ECB’s M2 money supply. Stabilization in peripheral bank deposits highlights the backstop that the ECB has put in place as a lender of last resort. Stability in the sovereign debt market is trickling down to the peripheral banking system. This is an incremental positive for European growth and it is beneficial to large-cap U.S. multi-nationals e.g. in the tech and industrial sectors.

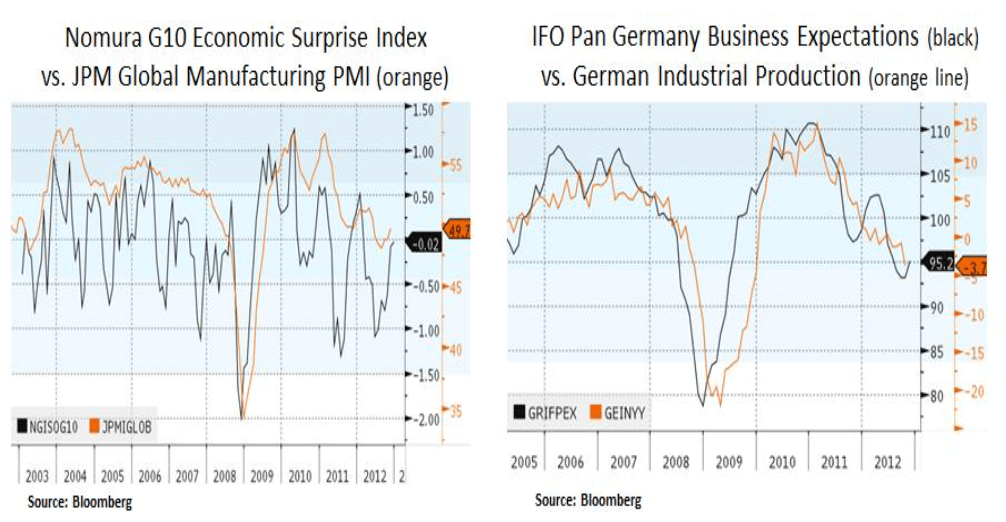

At the global growth level, there are tentative signs of stability. For export driven economies such as Germany, this may indicate better days ahead. The European economy is more leveraged to a global growth recovery. A fiscal resolution in the U.S. is the missing piece to a potential global growth recovery in 2013 and CEOs are looking for visibility before deploying their healthy balance sheets.

From a secular perspective, we continue to favor large-cap multi-nationals that are exposed to emerging market consumer spending growth. In particular, we like the relative safety of global pharmaceutical companies and late-cycle industrials with exposure to commercial aerospace and energy infrastructure.

In conclusion, we continue to assess the risk-reward profile of financial instruments across the fixed income and equity spectrum. We maintain our balanced portfolio approach with an income/late-cycle tilt. We favor instruments with visible cash flow and growing income streams.

Christos Charalambous CFA

Senior Strategist

christos.charalambous@edgewealth.com

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.