AI Funding Coming Under Scrutiny

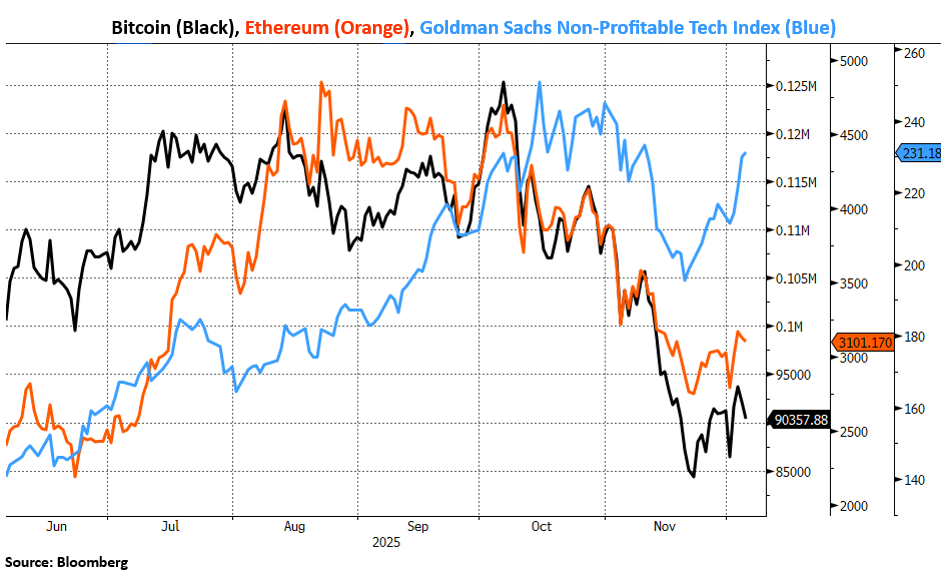

U.S. equities ended the month of November mixed, with the S&P 500 delivering modest gains, extending its winning streak to seven consecutive months, while the Nasdaq registered its first monthly decline since March. Market participants were faced with sharp mid-month volatility, a closed and then reopened U.S. government, incomplete economic data that showed mixed signals, and growing questions about the endurance of the artificial intelligence theme that has repeatedly carried markets to record highs. Investors witnessed a reshaping of AI leadership as some of those market leaders fell significantly, with investors growing increasingly concerned about potential circular financing risks tied to OpenAI and the broader AI funding ecosystem. There has been growing scrutiny around the sustainability of hyperscaler spending, financing structures, and competitive dynamics within the AI landscape. Companies that have massively expanded their reliance on debt issuance to support capital expenditures are being punished, marking a significant shift away from indiscriminate enthusiasm on “all things AI.” We also witnessed the enthusiasm around many “risk-on” trades moderate in November. The cryptocurrency market endured a meaningful correction triggering massive liquidations, levered ETFs saw net outflows, and other speculative cohorts fell significantly.

The rebound in stocks at the end of the month was driven largely by shifting expectations for a Federal Reserve interest rate cut at the December 10th meeting. Futures markets were pricing in less than a 30% chance after cautious Fed commentary early on, before climbing to almost 100% odds of a cut at the December meeting following dovish remarks from New York Fed President John Williams. Williams described current monetary policy as “modestly restrictive,” and suggested there is still room for further adjustments in the near-term to move policy closer to neutral (the interest rate at which monetary policy neither stimulates nor restrains economic growth).

Looking ahead, the outlook for risk assets and the U.S. economy will depend largely on whether the moderation in the labor market remains gradual and controlled. Long-term interest rates have been rising around the world, particularly in Japan where the Bank of Japan is expected to increase rates on December 19th. The Japanese bond market is currently experiencing significant volatility and upward pressure on yields. This is a result of expansive fiscal stimulus from the government, stubborn inflation, and hawkish signals from the Bank of Japan. Yields of Japanese Government Bonds (JGBs) have reached multi-decade or all-time highs, reflecting expectations of tighter monetary policy amid Japan’s ongoing efforts to normalize interest rates after decades of ultra-loose policy. Further rate hikes risk exacerbating yield spikes, slowing economic growth, and increasing debt-servicing costs for Japan’s massive public debt (debt-to-GDP ratio of nearly 230%). On the other hand, pausing or cutting rates risks accelerating inflation, which has exceeded the 2% target for 43 consecutive months. This is relevant from a global perspective because Japan’s actions could influence carry trade dynamics (borrowing money in a low-rate currency and investing in assets that offer a higher interest rate) and bond markets abroad, especially if the Fed’s rate path continues to diverge. August of 2024 serves as a recent reminder of how carry trade unwinds can cause substantial market turbulence.

When thinking objectively about the current government debt trajectory in both the U.S. and abroad, along with persistently sticky inflation, we believe the bias for long-term rates is higher. In light of this, we have shifted portfolios out of all preferred stock holdings which accounted for our longest duration exposure (price sensitivity to changing interest rates). Our short-term outlook remains cautious. While corporate earnings have remained solid and a lot of froth has come out of speculative areas of the market, the month-end rally in stocks was chiefly a result of shifting expectations around further rate cuts rather than improving economic momentum. Given that portions of the October jobs report will not be published as a result of the government shutdown, there will be considerable attention paid to the November jobs report from the Bureau of Labor Statistics on December 16th due to the heightened focus on labor market softness. We expect elevated volatility heading into year-end as investors recalibrate the principal drivers of equity returns and digest the evolving labor market picture.

We want to wish you all a happy holiday season.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product directly or indirectly referenced will be profitable, equal any corresponding indicated historical performance level, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. This content does not serve as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. If you have any questions about the applicability of any content to your individual situation, we encourage you to consult with the professional advisor of your choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request or by selecting “Part 2 Brochures” here.