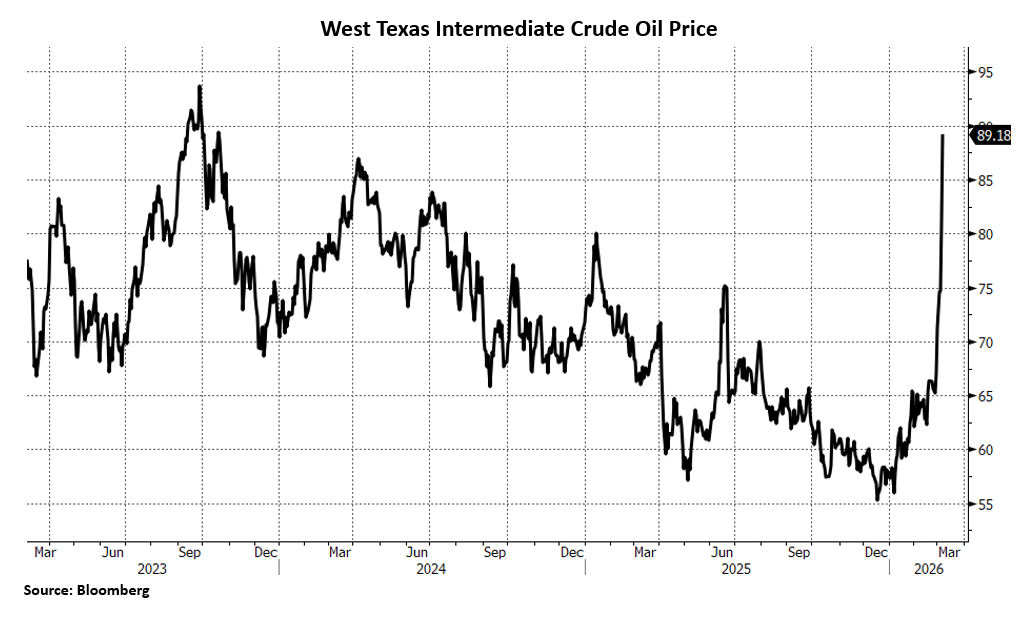

Middle East Conflict and Surging Oil Prices Fueling Global Uneasiness

The U.S. stock market has posted uneven, modest gains year-to-date amid a powerful sector rotation. Performance has been shaped by resilient domestic growth, geopolitical volatility, moderating (but persistent) inflation, jitters in private credit, and caution from the Federal Reserve. January began with optimistic momentum fueled by the prospects of strong earnings growth, Federal Reserve interest rate cuts, and tax cuts, all helping to lift the S&P 500 to a new all-time high. There has been a pronounced broadening of leadership away from mega-cap technology companies due to reassessments of software and AI valuations. The energy, materials, industrials, and staples sectors have all lead the way, while financials, communication services, and information technology sectors have all lagged.

Geopolitical developments have injected volatility into markets as the U.S. and Israel launched strikes on Iran over the weekend and have continued actively dismantling Iran’s military capabilities. Iran has retaliated against much of the energy infrastructure in the Gulf, and has effectively shut the Strait of Hormuz, the narrow sea passage in the Persian Gulf where roughly 20% of the world’s oil transits. This has sent oil prices surging, and has reignited concerns over inflation and the Fed’s ability to deliver interest rate cuts.

Following three 0.25% rate cuts in 2025, the Federal Open Market Committee held the federal funds rate steady at 3.50%-3.75% at its January meeting, citing a stabilizing labor market and inflation still above target. Fed Chair Powell emphasized the Fed would remain data-dependent and feels no immediate pressure to ease further. President Trump has formally nominated Kevin Warsh to serve as the next chair of the Federal Reserve’s Board of Governors when Powell’s term ends in May. Warsh’s path to confirmation in the Senate, however, faces hurdles. Warsh’s roadmap for future Fed action consists of lower rates centering on a technological revolution delivering a low-inflation environment, and a desire to shrink the Fed’s balance sheet. Most Fed officials see no compelling urgency for additional rate cuts as inflation is still elevated. The biggest surge in oil prices in four years stemming from the current conflict in the Middle East likely only adds to their disinclination. According to the minutes of the January Fed meeting, several officials have also considered the possibility that the Fed may need to hike rates should inflation stay above target.

This morning’s employment report for February showed an unexpected drop in payrolls of 92,000 according to the Bureau of Labor Statistics data, the largest decline since the pandemic. The unemployment rate climbed to 4.4%, and the labor force participation rate fell to 62%. These figures raise the question of how much the labor market is actually stabilizing, and could shift the Fed’s focus away from inflation and back onto jobs.

While credit spreads have widened over the last few weeks, we still view the risk/reward in credit as unattractive and continue to favor quality in fixed income, specifically Agency MBS and Investment Grade Municipal bonds. In Agency MBS, demand is regaining momentum, led by an increase in GSE purchases following government-policy support, a rebound in large-bank holdings, and strong taxable-bond fund inflows. We remain cautious on duration as the treasury market is resetting on inflation concerns about rising oil prices. Continued weakening jobs data could pull forward the timing and increase the depth of rate cuts on the front end of the yield curve, or meaningful upside surprises in inflation could renew the curve steepening on the long end. Overall, markets have remained resilient but cautious, supported by solid corporate earnings, yet tempered by high valuations, geopolitical uncertainty, and volatility. Markets across assets are actively repricing risk as investors weigh AI-driven disruption and capex, which have already led to sizable rotations in leadership within equity markets. The market’s current dynamics underscore the relevance of diversification, risk management, and the preference towards earnings quality.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product directly or indirectly referenced will be profitable, equal any corresponding indicated historical performance level, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. This content does not serve as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. If you have any questions about the applicability of any content to your individual situation, we encourage you to consult with the professional advisor of your choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request or by selecting “Part 2 Brochures” here.