Markets Recalibrate on Evolving Conflict in the Middle East

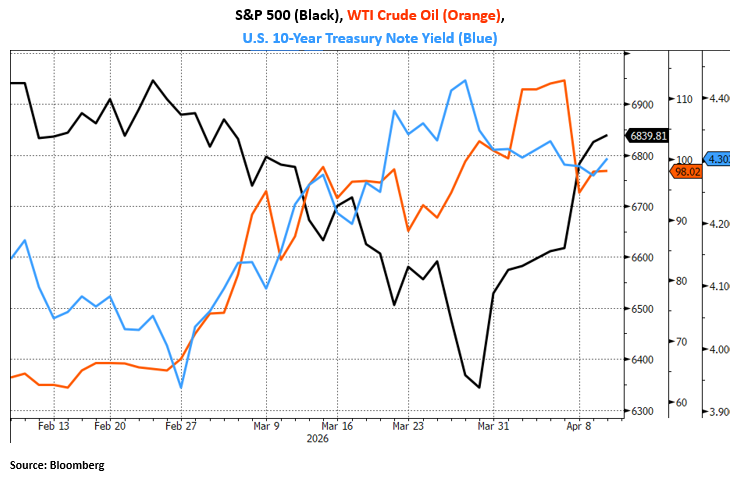

Geopolitical risk dominated the investment landscape in March as the escalating fighting in Iran and surging oil prices rattled investor confidence. The S&P 500 fell 5%, marking its worst month since September 2022, while international and emerging markets fared even worse, with the FTSE All-World ex U.S. Index sinking 11%, and the MSCI Emerging Market Index declining 13%. Sector performance reflected the oil-price shock: with Energy outperforming on higher crude prices, while Technology, growth stocks, and rate-sensitive sectors lagging amid higher yields and AI valuation concerns. Bonds also fell as Treasury yields rose sharply on inflation and policy repricing. The multi trillion-dollar Private Credit market continued to come under stress, with withdrawal limits being imposed from several major credit managers. Broadly, markets showed significant intra-month volatility, with considerable relief rallies on ceasefire headlines.

President Trump’s announcement Tuesday that he was accepting a proposal for a two-week ceasefire in Iran was met with jubilation in financial markets. Iran has showed little willingness, however, to accept US terms that would dismantle the remaining regime, or see the country follow Venezuela’s blueprint in elevating US-friendly leaders. For now, large portions of the Iranian Revolutionary Guard remain in place. Early indications are that those who remain are even more hardline than their predecessors, which may offer clues as to why negotiations to end the conflict have been mired in uncertainty. The Strait of Hormuz remains effectively shut to commercial traffic, as the surviving Iranian leadership has been able to weaponize the passageway to enhance their negotiating leverage. Without a clear off-ramp, the conflict may continue to hold markets hostage to every headline.

The FOMC met on March 17-18 and held the federal funds rate steady at 3.50%-3.75%. The statement noted solid economic activity, but highlighted elevated uncertainty from the conflict in the Middle East and oil shock. The Summary of Economic Projections, or “dot plot” projected one additional 0.25% cut for 2026, though several officials shifted toward fewer or zero cuts amid higher inflation risks. When the minutes were subsequently released, they revealed a growing willingness amongst the board to potential rate hikes if oil-driven inflation proved persistent, while Chair Powell emphasized a patient, data-dependent stance. The next Federal Reserve meeting is scheduled for April 29th, and expectations for any rate cut remain low at roughly 1%.

What remains to be seen for markets and the economy in the coming months are the effects on the cost of living resulting from the historically large disruption in oil supply. U.S. economic data has remained fairly resilient, and the positive tailwind of the One Big Beautiful Bill will begin to take effect after tax season. March marked a disorderly month for U.S. markets, but underlying economic resilience and potential conflict de-escalation offers hope heading into spring. The upcoming corporate earnings season could help equities find their footing after they have traded on news flow the last six weeks as opposed to fundamentals.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product directly or indirectly referenced will be profitable, equal any corresponding indicated historical performance level, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. This content does not serve as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. If you have any questions about the applicability of any content to your individual situation, we encourage you to consult with the professional advisor of your choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request or by selecting “Part 2 Brochures” here.