Sound Corporate Earnings Outweigh Tenuous Middle East Conflict

The major indices posted exceptional returns in April, with the S&P 500 and Nasdaq Composite both hitting fresh record highs and delivering their best monthly performances since 2020. This marked a sharp reversal from March’s drawdown as stocks showed notable resilience despite a fragile Middle East ceasefire backdrop. The rally was driven primarily by strong corporate earnings, continued AI momentum, and the aforementioned de-escalation signals in the Middle East. Large-cap technology leadership has retaken the reigns as renewed exuberance around artificial intelligence and associated infrastructure spending has dominated the headlines. Small-caps have also participated, with the Russell 2000 pressing up against all-time highs as domestic economic activity has remained robust.

The FOMC held the Federal Funds target rate unchanged at 3.75% at their April meeting, marking the third consecutive meeting without a change. There was notable dissent at the meeting, with one vote for a rate cut, while three others opposed the easing bias in the language. Fed officials remarked about elevated uncertainty from energy prices and geopolitics. Markets repriced expectations for rate cuts in 2026, and now see greater odds of rate hikes in 2027 amid sticky inflation. The Fed is approaching a leadership transition. Fed Chair nominee Kevin Warsh was confirmed by the Senate Banking Committee and the vote now moves to the full Senate, where his is expected to be confirmed ahead of current Fed Chair Jerome Powell’s term ending on May 15th. Powell has indicated that he plans to remain on the Board of Governors, and while the transition is expected to be orderly, it introduces a new dynamic as markets assess how Warsh’s leadership may impact monetary policy.

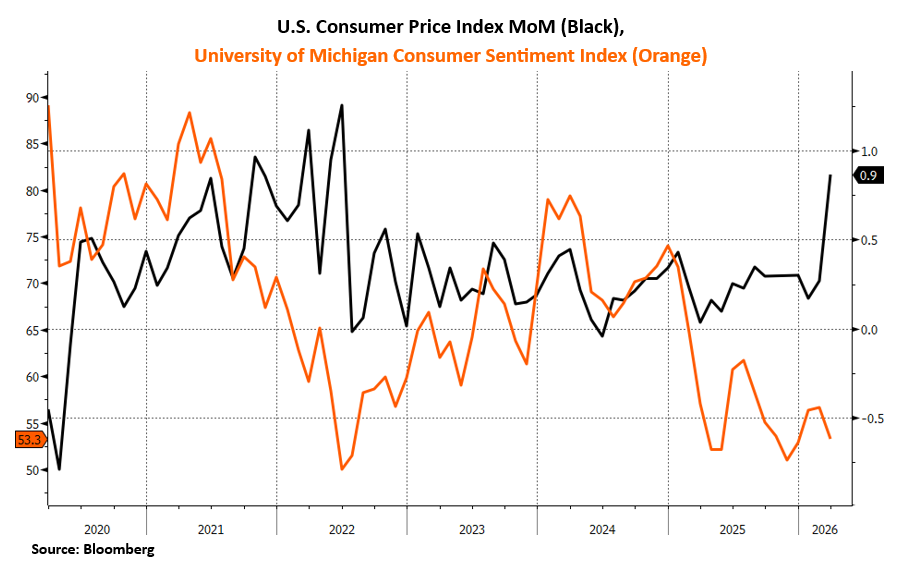

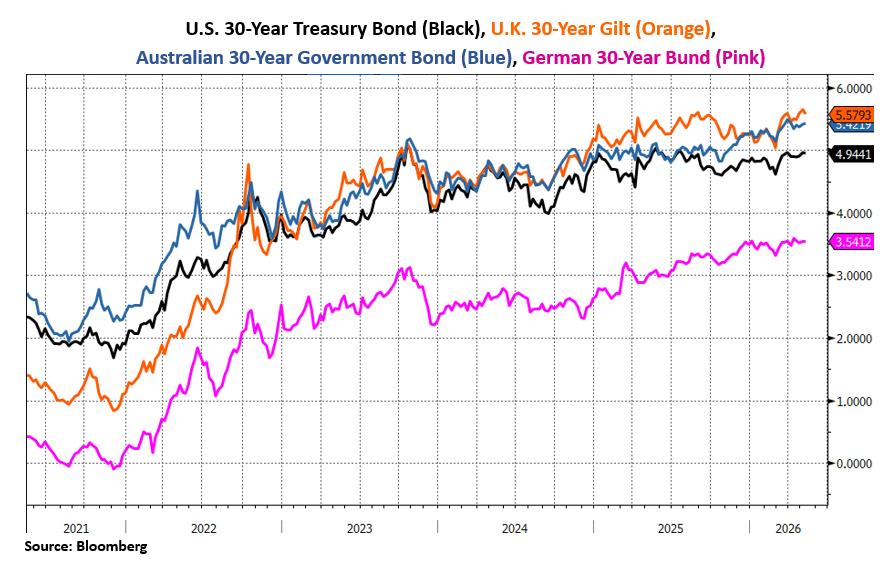

Economic data has been resilient broadly as the U.S. employment report for April released this morning showed employers adding more jobs than expected for a second month, and the unemployment rate held steady, indicating the labor market is holding up despite rising energy costs. Inflation rose in March by the most in nearly four years. The critical variable moving forward is whether the conflict in Iran, which has already driven prices higher and crushed consumer sentiment, will begin to weigh on the labor market. International bond markets have taken notice. Longer maturity bonds are often viewed as a proxy for inflation expectations, as the real value of the bond’s fixed payments in the future decreases, decreasing the bond’s current value. The U.K.’s 30-Year Gilt hit its highest level in yield since 1998, while the 30-Year U.S. Treasury and others are bumping up against their multi-year respective highs in yields.

We’re cautious on risk assets in the near-term given the rebound in equity markets over the last few weeks. The move has been supported by strong earnings and the AI supercycle, however geopolitical risks remain, and energy continues to put upward pressure on inflation. The margin for error is slim, however, given the precarious situation in the Strait of Hormuz and the ramifications that brings to the global supply chain. Compound this with the volatility that midterm election years typically bring, as well as the fiscal debt dynamics, and we may be in for a choppy summer. While we are wary of the current market setup, it’s possible equities can continue their march higher on the heels of sustained earnings growth and solid economic fundamentals.

Ryan Babeuf, CFA

Market Strategist

Ryan.Babeuf@EdgeWealth.com

Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product directly or indirectly referenced will be profitable, equal any corresponding indicated historical performance level, or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. This content does not serve as the receipt of, or as a substitute for, personalized investment advice from Edge Wealth Management, LLC. If you have any questions about the applicability of any content to your individual situation, we encourage you to consult with the professional advisor of your choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request or by selecting “Part 2 Brochures” here.